This is a real-life hedge fund case study that was submitted during a final-round interview for a New York City-based hedge fund. This case study was completed for a multi-billion dollar hedge fund.

The case study is 8+ pages and was pitched as a short investment in the Industrials sector. This was a very time-consuming and detailed process where the analyst spent a week building out his thesis and making the argument for a short position in this company.

Company: Cemex (Ticker: CX)

Recommendation: Short Equity

Company Description:

- CEMEX is the third-largest cement manufacturing company in the world, based on installed capacity of approximately 97.3 million tons (Lafarge and Holcim are the leaders).

- End market is infrastructure (65%) and the rest is new construction and housing.

- The company produces and distributes cement (49%), concrete (37%), and aggregates (14%).

- Operations in UK/Europe (31%), Mexico (21%), U.S. (20%), Central America (9%), Africa (7%), Spain (6%), and Asia (3%).

- EBITDA by Country: Mexico (47%), UK/Europe (19%), South America (20%), Spain (8%) and U.S. (6%) – with huge operational leverage in the U.S. market.

Situation

- CX is overly leveraged and entering a tough 2H with U.S. housing sales collapsing, fiscal tightening in the EU, and infrastructure budget cuts in Spain.

- I feel there is a decent chance that CX will bump up against debt covenants in the second half of 2010 if housing were to fall (when 2010 EBITDA falls below $2.66bn they break covenants, and they did already break with $2.80bn guidance in 2009).

What Is Your View?

- The company valuation looks rich—the company is trading at a +12% 2010 EBITDA premium to worldwide cement companies (+16% ’11, +18% ’12). Using my EBITDA estimate it’s trading at a +28% premium to 2010 EBITDA. The premium is not justified with such a weak balance sheet. Thus I do not think a covenant breach is being priced in, nor is any kind of 2H10 slowdown.

- Short interest is reasonably low – I think people truly believe in management’s guidance.

- Covenant talk is very public – they talk about it on every conference call and analysts are all well aware. Nobody is modeling a covenant breach because, in my view, everyone is way too high on their 2H10 assumptions. Citi’s model has 500bps EBIT improvement in 4Q10 YoY, which is just unrealistic.

- How it could this investment go against me? The big possibility here is asset sales, but then again, I don’t think CX is trading as if the company is going to break apart. Thus I spoke with Investor Relations (IR) about this – since they have minimum-operating restrictions from the covenants, selling EBITDA-generating assets won’t work. The company needs to start unloading non-EBITDA-generating assets. IR didn’t have a plan of attack on this at all, as they talked about some real estate in a Mexico JV worth ~$700mn and a few hundred million payable from the Venezuelan government. So even if they could sell off $1bn of assets it still doesn’t change the fact that EBITDA will miss by 30% in my view, and this scenario only takes the covenant breach possibility off the table—possibility that I don’t think is being priced in at all right now.

- I really don’t think analysts are focused enough around the covenant issue, but I could be wrong. Cemex just negotiated this financing agreement less than 12 months ago, and 2Q10 was the FIRST covenant test the company went through, so I doubt the company would already be negotiating different terms on this. I also think it would be a negative if the company re-negotiated this early –if it had to renegotiate terms this quickly, then the company is operationally falling apart, and estimates and stock price will have to come down.

2010 Guidance from 4/27/10 Earnings Call:

- EBITDA: On June 3rd CX updated EBITDA guidance due to exchange rate fluctuations of the euro/peso. Initially CX put out full year EBITDA guidance of $2.9bn and now expects $2.75bn (it breaks covenants at $2.66bn).

- Consolidated Volume: Cement +3%, Aggregates +1%, Ready-Mix to be “slightly lower than last year.”

- U.S. Volume: High Single-digits with increased volume from public works projects accounting for half this increase.

- Mexico Volume: Cement/Aggregates to decline by 4%, Ready-Mix to decrease by 8%.

- Europe Volume: Expects stabilization and potential growth.

- Spain Volume: Expected to continue declining.

- Asia Volume: Expecting a continued increase in cement volumes.

Price Increase

The first price increase did not stick, so announced another price increase in July of 11-12%.

American Recovery and Reinvestment Act (ARRA) Stimulus Outlays

The ARRA was enacted in 2009 as part of the economic stimulus package, intended to create jobs and promote investment and consumer spending during the recession. From the government site I have been tracking this on a weekly basis and I have a good feeling for the allotted infrastructure payments. 96% of the $27bn for highways has been obligated; out of this, only 26% has been spent in the entire U.S. at the end of April. In the states most relevant to CX, outlays are closer to 11-13% in states such as CA and FL. It could be that the states are just plugging their holes with the federal money – in that this is not incremental (i.e., if CA has an annual infrastructure budget of $100mn they are simply putting this on hold and taking federal stimulus dollars, so there could be no incremental sales volume here).

Leverage and Covenant Issues

CX’s balance sheet is overly levered with $17 billion debt while at the same time operations are falling apart.

At the end of 1Q10, CX was 6.4x levered (net debt/LTM EBITDA).

Per the company’s 20F, CX Breaks Covenants during:

- 2Q at >7.75x Total Debt/EBITDA or at

- 4Q at >6.75x Total Debt/EBITDA or at

As of 1Q10 CX was at 7.47x and 2.33x; I am currently modeling 2Q10 at 7.49x and 1.91x.

- If we see a big slowdown in U.S. housing and 2010 Margins fall to 7.0% (they were 8.0% in 2009) then there is a good chance CX will break covenants.

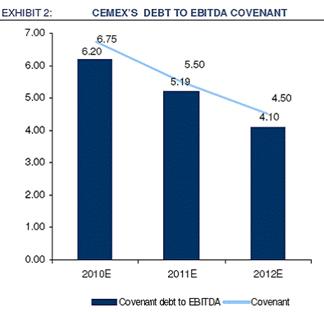

- As I showed above, Total Debt/EBITDA covenants reset from 7.75x in 1H10 to 6.75x in 2H10.

This is a look at full year 2010 estimates of margins vs. revenue; red shows a covenant breach (4Q10 covenants reset to 6.75x):

CX Breaks Covenants at 6.75x Debt/EBITDA or 1.75x Coverage

∆ in Total Operating Margin (Top Axis) vs. Revenue (Left Axis)

| 3.0% | 4.0% | 5.0% | 6.0% | 7.0% | 8.0% | 9.0% | 10.0% | 11.0% | |

| (15.0%) | 9.29x | 8.70x | 8.18x | 7.71x | 7.30x | 6.93x | 6.59x | 6.29x | 6.01x |

| (13.0%) | 9.25x | 8.65x | 8.12x | 7.65x | 7.24x | 6.86x | 6.53x | 6.22x | 5.94x |

| (11.0%) | 9.20x | 8.60x | 8.06x | 7.59x | 7.17x | 6.80x | 6.46x | 6.16x | 5.88x |

| (9.0%) | 9.16x | 8.54x | 8.01x | 7.53x | 7.11x | 6.74x | 6.40x | 6.09x | 5.81x |

| (7.0%) | 9.12x | 8.49x | 7.95x | 7.47x | 7.05x | 6.67x | 6.33x | 6.03x | 5.75x |

| (5.0%) | 9.07x | 8.44x | 7.90x | 7.42x | 6.99x | 6.61x | 6.27x | 5.97x | 5.69x |

| (3.0%) | 9.03x | 8.40x | 7.84x | 7.36x | 6.93x | 6.55x | 6.21x | 5.90x | 5.63x |

| (1.0%) | 8.99x | 8.35x | 7.79x | 7.30x | 6.88x | 6.49x | 6.15x | 5.84x | 5.57x |

| 1.0% | 8.95x | 8.30x | 7.74x | 7.25x | 6.82x | 6.44x | 6.09x | 5.79x | 5.51x |

| 3.0% | 8.91x | 8.25x | 7.69x | 7.20x | 6.76x | 6.38x | 6.04x | 5.73x | 5.45x |

| 5.0% | 8.86x | 8.21x | 7.64x | 7.14x | 6.71x | 6.32x | 5.98x | 5.67x | 5.40x |

Bottom Line: If we don’t see a U.S. housing recovery in 2H10 or 2011, CX will have to make drastic moves in order to avoid breaking covenants.

Quick Background on CX Covenants:

Under Cemex’s August 2009’s refinancing, CX’s debt covenants will be tested for the first time in June 2010, when its total funded debt is required to be no more than 7.75 times its last 12 months EBITDA. Cemex had a total debt including Perpetual Debentures of $19.458bn at the end of March 2010. The subsequent exchangeable offer for the Perpetuals reduced Cemex’s debt by $437m. I also estimate that Cemex generated a free cash flow in 2Q10 of $100-200mn, down from $323mm in 2Q09. I therefore expect it to report an end of June 2010 total debt of around $18.8bn. $614m of the $715m convertible issued in March is also included in Cemex’s debt, but is excluded under the banking covenants. I therefore estimate that its end-June total funded debt under the covenant will be around $18.2bn. it has US$6b in EUR-denominated debt, so EUR depreciation actually works in favor of reducing Cemex leverage multiples (and vice versa). We should see some of this in 2Q debt reduction.

Here’s the breakdown of all the smoke and mirrors that has happened during 2Q:

$19,458 (Total Funded Debt as of 1Q10)

Minus $437 (Exchangeable offer for the Perpetuals; this offering has closed)

Minus $200 (FCF Paydown; Guidance for FY $600mn Paydown)

Minus $614 ($614m of the $715m convertible issued in March is excluded from the covenants)

$18,207 (Total Funded Debt as of 2Q10)

There has to be a robust recovery for CX to avoid breaching covenants. In my model, Cemex is currently paying down debt from FCF of $1.0bn, $1.4bn, $1.4bn in 2010 through 2012. My model also grows operating margins to 8.7% in 2011 and 9.4% in 2012 (Reported 8.0% in FY09). Intra-quarter management cited leverage at 7.3x. Every 6 months, the covenants reset lower:

- September 28, 2009, CX sold a total of 1,495 million CPOs, directly or in the form of ADSs, in a global offering for approximately U.S.$1.8 billion in net proceeds.

- October 1, 2009, CX completed the sale of its operations in Australia to a subsidiary of Holcim Ltd. for approximately A$2.02 billion (approximately U.S.$1.7 billion).

- December 10, 2009, CX issued approximately Ps4.1 billion (approximately U.S.$315 million) in mandatory convertible securities.

- December 14, 2009, the subsidiary, CEMEX Finance LLC, issued U.S.$1,250 million aggregate principal amount of its 9.50% Senior Secured Notes due 2016.

- March 30, 2010, Cemex closed the offering of U.S.$715 million of its 4.875% Convertible Subordinated Notes due 2015.

- May 12, 2010, the subsidiary CEMEX España, acting through its Luxembourg branch, issued U.S.$1,067bn aggregate principal amount of its 9.25% Senior Secured Notes due 2020.

If Cemex is in breach of covenants at 4Q10, the company will need to solicit a waiver. Given that they completed the US$15b refinancing less than 1 year ago, have achieved 2009 and 2010 and milestones way ahead of schedule, and have continued to strengthen the balance sheet with equity issuance, convertibles, and divestitures, the company might be able to obtain a waiver in exchange for a normal fee.

Jefferies, who has a BUY rating on the stock, is modeling in 214bps of margin improvement in 2010 and 229bps in 2012.

This is absolutely a call on U.S. HOUSING coming back in 2011/12 – meanwhile, the infrastructure investment starts to wear off a bit in 2011, and by February 2012 all the ARRA money is supposed to have been spent!

If we model in a robust worldwide economic rebound, we’re still skating on very thin ice for the stock!

On the chart below, observe how close CX will to breaking covenants under a very positive economic rebound scenario:

Meanwhile, EBIT fell by 54% YoY in 1Q10. With a slowdown in U.S. housing, and budget cuts in EU/Spain, we’re looking at huge likely margin pressure in the back half of 2010:

Operating margins collapsed in 1Q10, falling to 4.9% from 8.9% in 1Q09. Meanwhile, the company has estimates for 2Q10 ranging from 7.0%-11.8% (note that the business model has changed a bit since 2005).

The chart below shows cement production (million tons) by country in which CX has sales.

Notice that US/Mexico/Europe make up 72% of revenues:

| 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | CAGR | ’08-09 | |

| Brazil | 35 | 36 | 39 | 42 | 47 | 52 | 52 | 5.8% | 0.0% |

| Egypt | 33 | 36 | 39 | 39 | 40 | 40 | 47 | 5.2% | 17.5% |

| France | 20 | 21 | 21 | 22 | 22 | 21 | 18 | (1.5%) | (14.3%) |

| Germany | 34 | 33 | 32 | 34 | 33 | 34 | 30 | (1.8%) | (11.8%) |

| Italy | 44 | 46 | 46 | 48 | 48 | 43 | 36 | (2.8%) | (16.3%) |

| Mexico | 32 | 33 | 37 | 39 | 40 | 39 | 37 | 2.1% | (5.1%) |

| Spain | 45 | 47 | 50 | 54 | 55 | 43 | 31 | (5.2%) | (27.9%) |

| USA | 93 | 97 | 99 | 98 | 96 | 87 | 72 | (3.6%) | (17.2%) |

| Total | 336 | 349 | 363 | 376 | 381 | 359 | 323 | (0.6%) | (10.0%) |

Source: CEMBUREAU Activity Report

CX has operations all over the world:

- Spain – Public works are a disaster, and the government has announced a plan to cut investment in infrastructure projects by 20% in 2010 in order to reduce its deficits.

- US – Everyone really bulled up from the ARRA spending and housing outlook – 2H estimates assume revenue growth and continued positive recovery in housing.

- Mexico – This is showing positive signs from a +4% YoY increase in mortgage originations during 2Q10 and positive remittance data in peso terms (an important driver for the self-construction segment).

- Note: Without a sustained economic recovery in the U.S., coupled with a recovery in U.S. unemployment, remittances are likely to remain weak this year and next, continuing to affect self-construction in Mexico. Moreover, if U.S. growth is weaker than expected and unemployment remains high, continued weakness on both commercial and middle and residential housing in Mexico could persist. With housing comes new communities that need cement roads, pipes, embankments, landscaping, social developments (i.e. village centers), etc.

Industry Data in the U.S. has been slightly positive from March-May but is starting to lose steam:

CX Valuation

CX is trading at 9.5x 2010 Consensus EBITDA. 2010 Consensus EBITDA is still way too high in my view, but look at the delta between implied prices below. If we apply a 9.5x multiple on my estimated 2010 EBITDA, we get an implied price of $5.50. We could even argue for a lower multiple; right now, CX is trading at a 10% premium to the worldwide cement producers based on EBITDA.

| Street | Our View | |

| Price | $9.35 | $9.35 |

| Shares | 998 | 998 |

| Mkt Cap | 9,335 | 9,335 |

| Debt | 16,587 | 16,587 |

| Cash | (748) | (748) |

| EV | 25,174 | 25,174 |

| ’10 EBITDA | 2,640.5 | 2,237.5 |

| Market Multiple | 9.5x | 11.3x |

| Implied Multiple | 9.5x | 9.5x |

| Implied Price | $9.35 | $5.50 |